Learn What is the Score for CIBIL?

Over the years, both the lenders and the borrowers have become important to the loan industry. It is, therefore, necessary for the lending authorities to be able to evaluate the worthiness of a customer in order to better manage the risk.

And they should be able to grasp the chances of their acceptance with regard to loan seekers. The CIBIL Score was therefore developed to encourage a healthier credit system for our country.

CIBIL stands for Credit Information Bureau (India ) Limited, India’s first Credit Information Company. It was founded in 2000 and has been a worthy participant in our financial system since then.

In addition, this organization manages the individuals’ credit information suggested by the organizations that are registered with them. Moreover, in conjunction with CIBIL, TransUnion, International Inc and Dun and Bradstreet serve.

CIBIL Score is a three-digit numeric outline of your record as a consumer. The score is inferred utilizing the record as a consumer found in the CIBIL Report (otherwise called CIR i.e Credit Information Report). A CIR is a person’s credit instalment history across advanced kinds and credit organizations throughout some undefined time frame. A CIR doesn’t contain subtleties of your reserve funds, ventures or fixed stores.

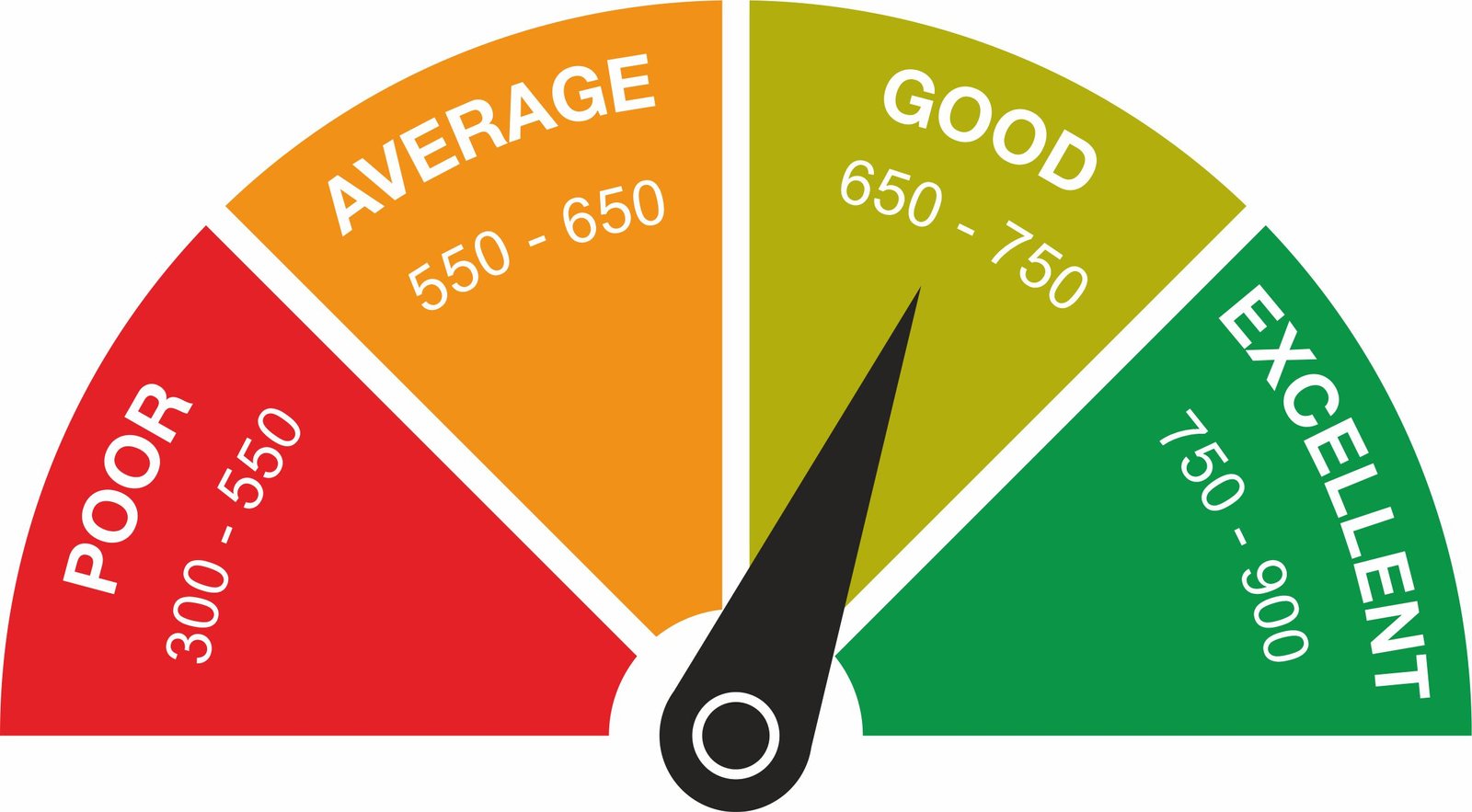

The Score depends on subtleties found in the ‘Records’ and ‘Enquiries’ segments of the CIBIL Report, including (however not limited to) advance records or charge cards, instalment situations with, sums and days past the due date. Going from 300 to 900, the nearer a CIBIL Score is to 900, the higher are the odds of the shopper’s Visa or advance application getting endorsed.

GOLD LOAN @ 0.75%*

APPLY NOW

What’s the Score for CIBIL?

In the banking industry, a high three-digit number that determines a person’s creditworthiness is proclaimed as The Credit Score or CIBIL Score. In order to get a loan, this score is not just a condition that a person must fulfil. In fact, this is the basis on which the approval of a loan is heavily dependent.

In order to authorize any loan, all lending institutions rely heavily on the Credit Information Reports that present the Credit Score. After taking comprehensive credit details into consideration, a Credit Score is produced. And, usually, the range is between 300-900.

What does a good and poor credit score mean to you?

Basically, a credit score is the indicator of the magnitude of paying the bank back the debts. You will have a decent credit score if you return your debts on time, i.e. your credit card bills or your EMI’s, otherwise, it will be poor. A good CIBIL Score projects the client’s responsible and good repayment conduct, which further encourages the lenders to create trust in them.

In order to get fast loan approvals or higher credit limits, a strong CIBIL score should therefore be maintained. The collection of scores deemed good or poor is here:

- Outstanding credit score-over 750.

- Good credit rating-Between 700 and 750.

- Bad credit rating-Below 550

Note: In the event that a person has not taken advantage of a loan, the credit score remains -11.

GOLD LOAN @ 0.75%*

APPLY NOW

How can I check my CIBIL Score?

To get a free CIBIL score online the customer can sign-in on the power website of the credit organization and request the report. Also, to get the report the customer needs to equip the essential files. It is solely after the confirmation of chronicles that the customer will get the CIR through email within a day. In any case, there is a basic and quick substitute where you can check the CIBIL score by PAN Card (just and no other documentation is required). In addition, you don’t have to pay any costs to get a free credit prosperity check.

You can Check CIBIL Score by PAN Card and Whatsapp

CIBIL Score can be checked through your PAN Card and Whatsapp by following the basic steps given below-

For PAN Card

- Go to the CIBIL score page

- Enter your Name according to PAN Card

- Notice right Date of Birth

- Select Gender

- Give PAN Card number

- Enter contact subtleties, for example, email address, residence address and versatile number

- Consent to the terms and condition

- Snap-on the submit button

For Whatsapp

- Give a missed call to +91-9878981166

- Versatile Number will be added to WhatsApp Chat

- Fill Your Name, Date of Birth and Gender

- Enter your PAN Number

- Give your total residence address

- Enter your Email ID

Important factors to maintain a Good CIBIL Score

- Keep a credit use extent under 15%–25% of your full-scale open credit.

- Make an effort not to default on your credit and repay your commitments on time.

- Make an effort not to open diverse development records immediately

- Check your credit report now and again and right any potential bumbles expecting any, this will improve your score.

GOLD LOAN @ 0.75%*

APPLY NOW

Effects of PAN Change on CIBIL Score

Along these lines, on the off chance that you change your PAN card or number, your Credit score assessment won’t be influenced. Credit score has different subtleties like your date of birth, banking exchanges, private location, and so on. Thus, on the off chance that your PAN number has been changed, at that point, the CIBIL programming will show an admonition in your record.

There are few factors that affect the Credit Score of an individual and they are as follows-

- Payment History-Making late payments or defaulting your EMIs or dues will negatively impact your score.

- High Credit Utilization- An increase in the current balance of your credit card indicates an increased repayment burden and may negatively impact your score.

- Credit Mix- Having a balanced mix between secured loans and unsecured loans is likely to have a more positive effect on your score.

- Multiple Enquiries- If you have recently been sanctioned multiple loans and credit cards, then lenders will view your application with caution because this behaviour indicates your debt burden has increased, which will negatively impact your score.

Factors Adversely Impacting CIBIL Score

Your creditworthiness can be influenced by the following variables:

- Re-payment History: Paying the bills on time plays a significant role in establishing a decent credit score, to begin with. If one has a good payment history, the lending institutions consider a person to be serious and capable of clearing existing debts. The credit score can be negatively affected by late credit card payments or irregular EMI payments

- Unsecured services: Next, while unsecured services are very impressive, your credit score may be affected by a high percentage of these loans. Hence, your credit score can be favourably influenced by keeping a decent balance of both secured and unsecured facilities.

- Credit Card Balance: In addition, if there is a rise in the current balance of your credit card, there will be a negative impact on the credit score. Therefore, since it raises the repayment burden, one does not maintain any outstanding credit card bills.

- The number of loans and cards: In addition, in comparison to those who take one loan at a time, an applicant with several credit cards or loans appears to have a lower credit score.

Multiple Number of Hard Queries: Ultimately, when a lender tests an applicant’s credit score, the word Hard Query is used. Many challenging questions may also have a negative impact on the credit score.

The CIBIL Score is created by a scoring calculation, which considers an enormous number of information focuses and full-scale level credit patterns. It depends on three years of financial record. Essentially, there are four key factors that sway a shopper’s CIBIL Score – instalment history, credit blend of got or unstable advances, enquiries and credit use. Notwithstanding, the most recent CIBIL Score calculation likewise incorporates the profundity of credit (that is, the length of your current record as a consumer from when your most established credit account was opened), long haul pattern of extraordinary adjusts, exchange history on Mastercards, the proportion of real reimbursement add up to aggregate sum due and new records opened/accounts shut.

You can calculate your EMI here: Personal Loan EMI Calculator

GOLD LOAN @ 0.75%*

APPLY NOW

Reasons why your CIBIL Score is important-

- Your CIBIL report is a synopsis of your present and past credit exchanges. Checking your report consistently additionally helps report and amend any disparities that have brought down your score through no flaw of your own.

- Monetary foundations and loaning stages consider a CIBIL score of 750 or more as ideal. Consequently, it is imperative to assemble a record as a consumer and get a score as it improves your qualified to apply for credit under incredible terms.

How much is a CIBIL score required for any Loan?

A CIBIL score has a reach somewhere in the range of 300 and 900. You ought to preferably have a score that is more like 900 as it causes you to improve bargains on advances and credit cards. By and large, a CIBIL score of 750 or more is viewed as ideal by most moneylenders. You can get an individual advance with a CIBIL of 750 or more.

The credit score you are having straightforwardly relative to the advance you will get. On the off chance that you have a decent credit score, that will mirror a decent blemish on banks, and there will be the chance you will get the advance on schedule.

A credit score is a gigantic factor in an individual advance. Notwithstanding, individual credit is unstable and security free. So moneylenders will for the most part really like to see the cibil score.

In the event that you are applying for a business matter advance, that will be gotten as guarantee free on the off chance that you are utilized or working together. In both, the situation you will get the credit will be around 680 – 700 at least or more.

The home advance is to some degree enormous. The credit score for the home advance is at least 550. In the event that you are having a cibil score of under 750 will likewise be thought of. For the advance’s endorsement, the credit score is the main factor, and you should check your credit prior to profit from the advance.

GOLD LOAN @ 0.75%*

APPLY NOW

How is it possible to increase your CIBIL score?

Next, if you want to use a loan or credit card but have been denied by some lending authority, stop applying for credit after rejection. Do not, then, submit immediately to some other lending institution. Wait for the scores to improve, in fact.

The low frequency of applications: Secondly, when a borrower applies for a loan, banks review their credit score. Therefore, applying too many times for a loan or credit card could lower your credit score and show a person’s credit hungry actions.

You can improve your CIBIL Score by keeping a decent record, which is fundamental for credit endorsements by moneylenders. Follow these 6 stages which will help you better your score:

- Stop settlements on loans or credit cards: First, often people want to pay the balance of the loan or credit card bills. In other terms, an arrangement is reached between the borrower and the creditor in order to close the debt at a lower sum. The settlement is reflected in such situations on the credit report, which has a further negative effect on the credit score and also makes the banks unable to provide new credit.

- On-time Payments: In addition, the repayment of debts should be given priority by the claimant. In order to increase your ranking, if you miss the payment of your bills, make it a point to pay on time. Also, with the aid of the bank, the applicant may restructure the EMI plan to prevent any delay in payments.

- Take different forms of loans: In addition, borrowers can not only benefit from unsecured facilities. An individual can combine both secured resources such as a gold loan and unsecured loans such as personal loans in a balanced manner.

- Timely Credit Card Bills Payment: In addition, a person should avoid using the maximum card limit. This can reduce a person’s credit score. And always strive to pay either the full amount owed on the credit card or at least a significant part of it.

- Stop being a co-applicant: Often, even if he is not at fault, a person has to suffer. In such a situation, you are deemed at fault even though the loan seeker has not paid the amount. Which decreases your credit score even further.

- Continuously satisfy your obligations on schedule: Late instalments are seen adversely by loan specialists

- Keep your equilibriums low: Always be reasonable to not utilize a lot of credit, control your usage.

- Screen your co-marked, ensured and shared services month to month: In co-marked, ensured or mutually held records, you are expected similarly to take responsibility for missed instalments. Your joint holder’s (or the ensured singular) carelessness could influence your capacity to get credit when you need it.

- Survey your record as a consumer often consistently: Monitor your CIBIL Score and Report routinely to evade horrendous amazements as a dismissed advance application.

- Apply for new credit with some restraint: You would prefer not to mirror that you are persistently looking for unnecessary credit; apply for new credit mindfully.

- Keep a solid blend of credit: It is smarter to have a sound blend of got (like a home advance, automobile advance) and unstable advances (like individual advance, charge cards). Such a large number of unstable credits might be seen contrarily.

GOLD LOAN @ 0.75%*

APPLY NOW

How long does it take to improve the CIBIL Score?

Improving your credit score assessment is anything but a short-term measure, it requires both time and tolerance. There is no simple method to improve or fix your financial assessment. In this manner, getting fretful subsequent to seeing your low credit score rating is certainly not an exit plan, however, applying the right methodology in getting it expanded will be a shrewd and capable choice.

Individuals with low credit score rating by and large experience issues in getting an advance endorsed under their own name or deal with the issue profiting of another charge card, as every single monetary foundation altogether checks your credit report and explicitly credit score assessment, prior to offering you any loaning item. An awful or low credit score assessment can hamper your reliability and can additionally expand your monetary issues.

Your credit score rating is expanded or diminished on account of a few elements, for example, obligation sum, instalment history, new credit and length of credit. Your financial assessment is quite possibly the main factors that decide your reliability, particularly when benefiting from an advance. A decent financial assessment will make your credit application measure more straightforward and faster.

It is fitting to have your financial assessment checked, prior to applying for the credit application. This is since, supposing that the cibil score is less, you can pursue improving it, which will build your odds of credit endorsement. To improve credit score rating typically takes somewhere in the range of 4 a year relying upon your individual circumstance. For the most part, Credit Score over 750 is suggested. On the off chance that your score is on the lower end and under 600, it will normally require a significant stretch of time to expand your score to 750.

Factors Deciding Your Credit Score

A decent credit score is an approach to get faster support for your development or credit card applications. It is a huge factor that helps banks and non-banking account associations (NBFC) pick whether you are in a circumstance to repay the credit. A credit score is a numeric once-over that is gotten from your development reimbursement direct.

There are few factors that affect the Credit Score of an individual and they are as follows-

- Payment History-Making late payments or defaulting your EMIs or dues will negatively impact your score.

- High Credit Utilization- An increase in the current balance of your credit card indicates an increased repayment burden and may negatively impact your score.

- Credit Mix- Having a balanced mix between secured loans and unsecured loans is likely to have a more positive effect on your score.

- Multiple Enquiries- If you have recently been sanctioned multiple loans and credit cards, then lenders will view your application with caution because this behaviour indicates your debt burden has increased, which will negatively impact your score.

GOLD LOAN @ 0.75%*

APPLY NOW

Advantages of Good Credit Score

- Quick Loan Approvals: To begin with, the approval of the loan is carried out within a few hours if a person has a good credit score. The validity of the loan applicant is predicted by this ranking. Hence, enabling the client to trust the banks and NBFCs.

- Promotes loan eligibility: Next, the majority of banks depend on the applicant’s credit score. A good credit history thus increases the applicant’s eligibility.

- Better interest rates: Another benefit is that interest rate rebates are offered to individuals who have a decent credit score. A healthy Cibil Score thus positions an individual in a position to negotiate for a lower interest rate.

- HIGH CREDIT LIMIT: If an individual has a credit score greater than 750, it means that the applicant is a responsible borrower. Thus, greater credit card limits and better rewards are offered to you.

- Longer tenure option: In addition, individuals with a higher credit score may request a longer tenure on the loan. Interestingly, an outstanding Credit Score will help to extend to 25 years a loan term of & years.

- Better Benefits and Rewards: Eventually, a person with a high credit score will receive several benefits and rewards from credit cards. This provides keys to the world-class lounge, as well as miles of travel rewards.

Click here to know more about personal loan eligibility

How is the CIBIL score calculated?

CIBIL score online is determined by different credit departments utilizing their own restrictive calculation, however, the primary components of score organization rotate around the advance and Mastercard reimbursement conduct of a person.

- Financial record: Your previous credit reimbursement history or your financial record is of the greatest significance in the CIBIL score computation. Your previous credit history has a weightage of around 30% in the equation for computing your CIBIL score on the web.

- Credit Utilization: Your present extraordinary advance commitments partitioned by your accessible breaking point is utilized to ascertain the level of your credit use. The credit use proportion has a weightage of 25% in your CIBIL score count.

- Credit Mix: Your advance portfolio piece as far as the extent of got and unstable advances additionally has a direction on your score. A higher extent of unstable advances in your all-out advances portfolio has a negative bearing on your credit score assessment. Credit Mix is assessed to have a weightage of 25% in your score count.

There are other factors too. In the event that your CIBIL report shows different advance applications that have been dismissed in the new past, it gets reflected in a lower financial assessment. Banks are additionally unwilling to loan to borrowers, who have been dismissed by different banks. These different components are assessed to have a weightage of up to 20% in your CIBIL score estimation.

GOLD LOAN @ 0.75%*

APPLY NOW

Can inquiries impact your CIBIL Score?

A credit score is maybe the biggest influencer of credit endorsement or dismissal. Not simply that, it likewise impacts the expense of acquiring, how much an individual can get, and how adaptable the advance terms are. This is valid for all types of credit, be it gotten or unstable. A ton of elements are represented while figuring a person’s credit score assessment. While reimbursement narratives and Credit Utilization Ratios structure the biggest parts of the pie, the absolute exceptional credit balance, number of credit records, and agency requests are huge parts also.

Borrowers have frequently offered the conversation starter of whether different requests contrarily sway their CIBIL score. All things considered, the appropriate response is YES – various credit requests do antagonistically affect purchases credit score.

How do I read my CIBIL Report?

A CIBIL report has complete data on the credit you have profited, like a home advance, car advance, Visa, individual advance, overdraft offices.

- CIBIL Score

Your CIBIL score, determined dependent on your acknowledge conduct as reflected in the ‘Records’ and ‘Enquiries’ segment of your CIR, ranges between 300-900. A score over 700 is for the most part thought to be acceptable.

- Individual data

Contains your name, date of birth, sex and ID numbers like PAN, visa number, elector’s number

- Contact Information

Address and phone numbers are given in this segment, up to 4 locations are available

- Business Information

Month to month or yearly pay subtleties as announced by the Members (Banks and Financial foundations).

- Record data

This part contains the subtleties of your credit offices including the name of banks, sort of credit offices (home, auto, individual, overdraft, and so on), account numbers, possession subtleties, date opened, date of the last instalment, advance sum, current equilibrium and a month on month record (of as long as 3 years) of your instalments.

- Enquiry Information

Each time you apply for an advance or charge card, the individual Bank or monetary foundation gets to your CIR. The framework makes a note of this in your record and the equivalent is alluded to as “Enquiries”

GOLD LOAN @ 0.75%*

APPLY NOW

What do the various terms used in the Credit Information Report (CIR) mean?

- What are the principles of the Credit Information Report?

To obtain the loan properly, you should keep track of the bank history update the Credit Information Report. There are some terms you should know about the CIR.

- Actual payment amount

If the amount is different from the EMIs, you have paid, considered as an Actual payment amount.

- Amount overdue

The amount’s repayment has not been made to the lender, including the interest rate and the principal amount.

- High credit

High credit includes the highest amount of bill in your crest card, including the interest and the principal.

- Cash limit

The amount of cash you can withdraw from your credit card as if you apply for the credit card specifically.

- Control number

If you want to increase the dispute request, this is mandatory as the report number.

- Credit limit

The credit limit is the total number of credit cards you have access and in the credit card or overdraft facility.

- Ownership

Ownership is the details showing the lender who will have to pay the loan or credit card dues. Ownership includes the four categories like

- Single

The single person is responsible for paying the loan or credit bills. Single ownership will be going to reflects on your CIR

- Joint

Joint will include you, and one more person is responsible for the paying of bills. Joint will reflect on both the persons CIR.

- Authorised user

In this, the lender can quickly identify if you are paying the amount in the particular account. The Authorised user is used for adding up the credit card you are having apart from that.

- Guarantor

On behalf of someone else will be paying the loan. If the first person is unable to pay the amount, the other person has the responsibility.

- Settled Amount

When in an account, the amount is disputed. In settled amount, this will set the metaphor amount to pay as per the settlement of both.

GOLD LOAN @ 0.75%*

APPLY NOW

Why are the loans for which I am the guarantor showing up on my account

The unfortunate record and the low cibil score will be going to place you in a tough situation monetarily. At the point when you will profit from the advance, the moneylender will check your record. Notwithstanding, when you simply need to chip away at the record as a consumer and reimbursement of the credit. However, at times, things will end up being unique. You will not be able to pay the advance, and when you go for another, that will be a hazardous condition for the moneylender to profit you of the credit.

The underwriter is somebody who is the relative of the individual who profited the credit. Because of the low cibil score and the danger of request, the individual requests that the nearby individuals stay as an underwriter. At the point when the individual doesn’t pay the advance on schedule, the loan specialist will pursue the underwriter. In the event that you are over 21 years of age, you can be an underwriter, and that individual is more likely than not to be monetarily solid.

The terms when both the borrower and the underwriter will be not able to pay the credit will make bedlam. The upstanding instalment will be an inconvenient encounter as the bank may make a legitimate move against you. There may be the repossession of the resource you are having, and the FICO assessment ends up being less. The following time when you will apply, the moneylenders won’t be going to authorize the credit.

How to improve the CIBIL score with a personal loan?

Numerous individuals don’t know that taking care of individual advances in a trained way can help your credit score. Allow us to discover how –

Fabricate a decent instalment history – consistently make your own credit instalments on an ideal opportunity to assemble a decent instalment history. Solid instalment history can decide your credit department score. Continuously make sure to make the instalments in full each month. Standard Chartered encourages its clients to construct a decent instalment history by permitting its clients to set up robotized instalments. Discover more!

Lower your credit use – Credit use alludes to the amount you owe as far as possible on your credit card(s). Most grown-ups have a blend of rotating credit extensions including high-interest credit cards. Adding an individual advance to the part can diminish the credit use score and influence the credit score emphatically.

Improving the credit blend – the credit-scoring equation assumes the acknowledgement blend into account. Credit blend is the expansion of the various sorts of advances or lines of credits you are right now paying off. Including an individual advance along with the blend can decidedly affect your credit score as it shows that the individual has the insight into taking care of various sorts of credit.

How can a Gold Loan affect one’s CIBIL score?

Gold is quite possibly the most considered advance with regards to a got one. The gold credit is given by the NBFCs and public and private banks. At a sensible financing cost, you can get a gold credit. There are numerous reimbursement choices for the gold advance, including the EMIs and the overdraft office. The system to profit from the advance is likewise least. The gold advance gives an adaptable residency to the client to reimburse the cash

The reimbursement will influence history on the off chance that you are doing it at a specific time consistently. The instalment consistency will help you support the credit score, particularly on the off chance that you are going low on your credit score. You are paying the gold advance consistently to improve the credit score

At the point when you are having different credits and are unfit to pay them on schedule, the cibil score will go down according to this sort of circumstance. There are advances that you can profit from, yet the circumstance is by one way or another distinctive with regards to the gold advance. Having a credit score of under 500 can likewise profit the gold advance; the cash they are getting will be up to 75% greatest. It will be smarter to pay the cash on schedule and improve the credit score on the off chance that you can’t pay the remarkable advance.

Nonetheless, taking the credit and submitting it before the finish of residency will profit the borrower when making the gold advance.

GOLD LOAN @ 0.75%*

APPLY NOW

Do you need a CIBIL score for a personal loan?

An individual credit is an unstable or unprotected advance that doesn’t need the client to promise any sort of guarantee. The advance is endorsed in the wake of investigating the credit history of the client. This is the place where the CIBIL score has its influence. TransUnion CIBIL Limited additionally alluded to as the Credit Bureau of India is an RBI authorized organization that keeps up records of instalments identified with advances and credit cards.

A CIBIL credit score for an individual advance is a 3-digit number going from 300 to 900 that represents the credit history of the client. At Fullerton India, the higher your CIBIL score, the better are your odds of credit endorsement. Additionally, the endorsed credit sum relies significantly upon how great your CIBIL score is. Peruse more to think about the approaches to get an individual advance for a low CIBIL score.

The base CIBIL score for an individual credit is normally viewed as somewhere in the range of 720 and 750. Having this score implies you are creditworthy and moneylenders will support your own advance application rapidly. They may likewise offer you your picked advance sum at an ostensible interest.

Tips to get a personal loan despite a low CIBIL score

The cibil score is the constituent that is utilized for knowing the creditworthiness. Nonetheless, To get an advance rapidly, the credit score will be one of the elements. To keep a decent credit score is the main deed.

Prior to benefit from the credit, you should need to experience the very best banks giving the advances. Some of them will request you for more credit scores with a most extreme sum from cash. The other will attempt to acknowledge the credit score, which is low, yet the loan fee will be high. For instance, 550 to 600, at that point the moneylender attempts to ask you for more premium, and the odds of the advance will be less contrasted with the high credit score.

The moneylender may help you on the off chance that you don’t have a decent credit score. As you are acquiring and you are getting a sensible compensation on schedule. You can without much of a stretch convince the moneylender by talking about the compensation and the pay and augmentations you will get. In the event that the bank is persuaded that you are having less credit score, however, having a great job and pay will assist you with getting the advance. Be that as it may, it won’t be the conventional method to get a credit

A low credit score will indicate your record’s wellbeing, putting forth you make more attempts to ask the moneylender straightforwardly.

Importance of cibil score in personal loan

Individual advances have arisen as a mainstream choice for borrowers because of their simple application measure, quick preparing and snappy disbursal. Individual credits are unstable in nature for example they are not upheld by any guarantee, dissimilar to a home credit or a vehicle advance. Henceforth moneylenders give close consideration to a candidate’s credit score while assessing individual advance applications. The majority of the loan specialists check your CIBIL Score rather than a score by other credit agencies. Consequently, having a decent CIBIL score is basic for the endorsement of an individual credit application.

Your credit score assumes a significant part in the individual advance endorsement measure. The higher your credit score (commonly 750 and higher for example more like 900), the higher will be your odds of getting affirmed for individual credit. While having a low credit score doesn’t naturally prompt dismissal of an individual advance application, it might effortlessly prompt your advance being endorsed with a higher loan fee or with a lower limit.

Moneylenders particularly incline toward high credit score if there should arise an occurrence of individual advance since it is an unstable advance and a high score normally shows a lower danger of default. As there is no insurance joined to your credit sum, in the event that you default it is extremely unlikely the loan specialist can recuperate the cash from you. Subsequently, loan specialists demand high credit score for example people with a lower danger of not taking care of the sum acquired.

The CIBIL score ranges somewhere in the range of 300 and 900. The nearer an individual’s score to 900, the higher will be their odds of getting an individual advance endorsed. Albeit various banks have various standards for affirming an individual advance, by and large, a credit score that is more like 900 for example 750 and higher is viewed as a decent credit score.

GOLD LOAN @ 0.75%*

APPLY NOW

Impact of CIBIL score on a personal loan

An individual credit is an unstable advance that won’t be constant in asking you for security. The advance which will take just relies upon the credit score you are having. The credit score for the smooth and simple endorsement should request a high credit score. To put it plainly, the bank will be going to check whether you are reliable or not.

The credit score’s five critical constituents are credit history, credit blend, Payments history, all-out obligation, and new credit. The credit history is some way or another said to be the historical backdrop of the record. In which you have taken, the loan specialist’s cash will appear. The credit blend is the sort of record that keeps your credit record—the credit blend structures up the FICO score of about 10%. A few sorts of credit may be important for your credit blend, including contract, vehicle advance, home advance and many. The credit blend assumes an imperative part in the credit score and the dissipated credit history

The credit score is one of the fundamental pieces of the advance. The moneylender will check the creditworthiness of you and afterwards give you the advance. The credit score some way or another may drop down because of certain reasons like a hard request. This is the point at which numerous moneylenders will check the historical backdrop of the record. At the point when you have applied for such countless advances at a solitary time, Will prompts a hard request, which will influence the cibil score. The hard request will drop down the cibil score by 5-10 %. At the point when you are steady about the reimbursement, you will tally the 35% and make around this much score. Along these lines, the reimbursement of the advance will be valuable to the credit score.

How much Personal Loan amount can I get according to CIBIL?

In an individual advance, we take a financial sum from the financial establishments. At the point when we need cash, we approach banking organizations. They check our own and expert records. After confirmation, they recognize the sum which can be given to us as advances. While giving us the advances, they break down the entirety of our reports cautiously.

Individual Loan Amount with CIBIL Score of 720-750

In the event that there is an inopportune instalment of the advance, the CIBIL Score rating would be beneath. With a CIBIL Score of 720-750, you can take an individual advance of 5,00,000-10,00,000. Along these lines, the previously mentioned CIBIL Score would be sufficient for you to take the advance.

Individual Loan with CIBIL Score more than 700

CIBIL Score of more than 700 likewise brings you the chance to profit from individual advances like Business Loans. On occasion, the advance sum is important for setting up and building up a business.

At the point when you have a CIBIL score of more than 700, you can benefit from a business advance from the financial foundations. The second class of advances that can be contemplated is home credits. For benefiting from home advances, you require a specific CIBIL Score. Home Loans profit when you need to purchase private property. You can either buy a house or a level as per your ability. You can take credits from the financial foundation while buying such private foundations. On the off chance that you have a CIBIL score of around 550, you can buy a private foundation. Your CIBIL score would help secure home credits. Further, you can utilize this financial add up to fabricate a house or some other private foundation as per your necessities and wants.

CIBIL Scores are a vital rule deciding your advance taking a limit. Individual Loans are impacted by CIBIL Scores.

Can you get a personal loan with a low CIBIL score?

Credit score, however it has been around for some time, has become well known as of late. However, an enormous piece of the populace doesn’t think about credit scores or the way that they have one.

Out of nowhere, at some point, while applying for an advance, the bank reveals to them their credit score is low and that their advance application has been dismissed because of that.

At the point when you have a low score, it implies that you are a hazardous client and banks are generally not able to give you an advance. A credit score is fundamentally founded on how well you have reimbursed your past advances, regardless of whether you have defaulted or pre-shut any advance, what kinds of advances you have taken and the amount of your pay goes in reimbursing advances.

Along these lines, presently on the off chance that you have a low score and still need an individual advance, you can discover a few loan specialists who will actually want to give you the cash, yet they for the most part charge a high pace of revenue. A few loan specialists even energize to 30-40% p.a., which is exceptionally high.

In spite of the fact that it could be a test, with a low CIBIL score, you can get individual credit. There are numerous new emerging fintech stages and NBFCs that will offer you an advance yet may charge a higher loan fee.

Continuously research the moneylender and check whether they are trustworthy. Try not to fall prey to con artists who take your information and never dispense your advance. A few tricksters may considerably offer you incredible terms and conditions, yet they will make you pay a few charges in advance. You won’t ever see them or your cash again.

Guarantee you realize the right financing cost that you are getting. A few loan specialists may give an off-base picture by showing their financing costs as far as months and not years. Along these lines, 30% per annum is shown distinctly at 2.5% each month. Though an ordinary bank will charge you just around 14% p.a. which is just 1.66% each month. At the point when you ascertain interest throughout an extensive stretch of time, it adds up to a critical distinction.

GOLD LOAN @ 0.75%*

APPLY NOW

Benefits of a High CIBIL Score for Personal Loan

The two ideas which we have in the conversation here are Personal Loan and CIBIL Score. Right off the bat in close to home advances, you profit advances from banking organizations. At the point when you require reserves, you approach banking establishments. Banks investigate your archives altogether. After completely breaking down the archives, they decide if you are reasonable for tolerating the credit application.

As you take various assortments of advances, your assessment on the changes. With each passing chance, you find out about how to manage individual advances. Improvement of credit blend and the advance bin is critical. Hence your assortment of credits would assist you with lessening your monetary reliance on one advance inside and out.

It helps in building up an instalment climate. At the point when you take credits and reimburse them, an exchange happens. With an ever-increasing number of exchanges, your credit rating creates. As an exchange and instalment history is made, your dependability in the market improves.

Taking credit to meet your monetary necessities is acceptable. It is additionally a vital practice. Yet, it ought not to turn into a propensity. At the point when it turns into a propensity, you can’t limit yourself from assuming praise.

The more advances you take from the business banking foundations, the more costs you need to cause. The costs allude to the ones which are essential to tidy up the vital credit measure. Banking establishments charge the costs. Costs like Noting Charges for the bank move are considered in such a manner. The extra charges and costs vary starting with one financial establishment then onto the next.

In this manner, the previously mentioned focuses are imperative to comprehend the effect of individual advances on CIBIL Score.

How does Your Credit Score determine Your Personal Loan Interest Rate?

Your credit score rating is the biggest influencer in a private home loan endorsement. It grandstands how responsible you’re with money and in case you’re equipped for paying a loan specialist again on time without issue. The better your credit score rating, the more prominently honest your appearance to creditors. The best credit score rating is 850. To creditors, you will be the best possibility to get a home loan when you have a credit score rating that high.

By and large, a critical pastime charge for an individual credit is one. It is a decline than the nationwide normal, that is 9.41%, with regards to the greatest current to have Experian information. Your credit score rating, obligation to-income proportion, and various components all direct what leisure activity charge gives you may expect to gain. Be that as it may, it is likewise basic to appearance past interest while looking at individual credit choices.

Regardless of whether you have a credit score playing a game of cards or researcher advances, make a base insignificant bill every month. Doing so should diminish your obligation load even as furthermore developing a healthy value history. On the off chance that your credit score is on the decline side, you might need to get a credit scorecard. Whenever you’ve affirmed you’re responsible, you may show up utilizing a standard credit scorecard.

On the off chance that you definitely know an individual with an exact credit score, inquire as to whether you may arise as an authorized client on their credit scorecard. This is a direct way to support your rating without getting a credit score card or advance yourself.

Your credit score rating is perhaps the best technique to show your creditworthiness for banks and various creditors. Make positive you actually build your credit score, despite the fact that it’s now mistaken standing. On the off chance that it’s not, compositions on techniques to support it are snappier, so while it comes time to get an advance, your leisure activity expenses may be pretty much nothing.

To check Personal Loan Interest Rate for all major banks you can visit: Personal Loan Interest Rate.

Learn more at Dialabank and apply for the loans you need